The Bill You Never See

Gross ACA benchmark premiums rose 26 percent for 2026. Then the enhanced tax credits expired. The employer health subsidy nobody touches is why both fights miss the point.

You opened the renewal notice and the premium had a new number on it. Bigger. Maybe close to double. You did not switch plans. You did not get sicker over the holidays. The price went up while you were asleep, and nobody called to walk you through why.

The why is documented. Start with the receipts.

The enhanced premium tax credits that made marketplace coverage affordable for the last four years expired on December 31, 2025. KFF projected that would push subsidized enrollees’ out-of-pocket premiums up about 114 percent on average for someone who keeps the same plan, roughly a thousand dollars more a year. The real-world average came in lower, closer to 58 percent, because plenty of people fled to cheaper, higher-deductible plans or dropped out entirely. Read that second number as the size of the flinch. The sticker price climbed underneath that too. Unsubsidized benchmark premiums rose 26 percent on average, the biggest jump in eight years.

That works out to more than 20 million people facing a bigger bill. KFF now estimates marketplace enrollment could fall from 22.3 million in 2025 to about 17.5 million in 2026.

The line you are hearing is that one side could not repeal the ACA, so it let the help quietly run out instead. That part is real. The enhancement passed on Democratic votes in 2021. It was allowed to lapse, and the credit math was tightened, on Republican-controlled terms. So name the room. But the room is not the whole house.

Walk down the hall to the other system, the one most working people actually use.

In 2025 the average employer family health plan cost $26,993. The worker saw $6,850 of that leave their paychecks. The employer covered the rest, about $20,143, KFF found. The employer is not eating that money. Economists who study this for a living agree the company gets it back the boring way, by paying you lower wages than it otherwise would. You never see the bill because it shows up as a raise you did not get.

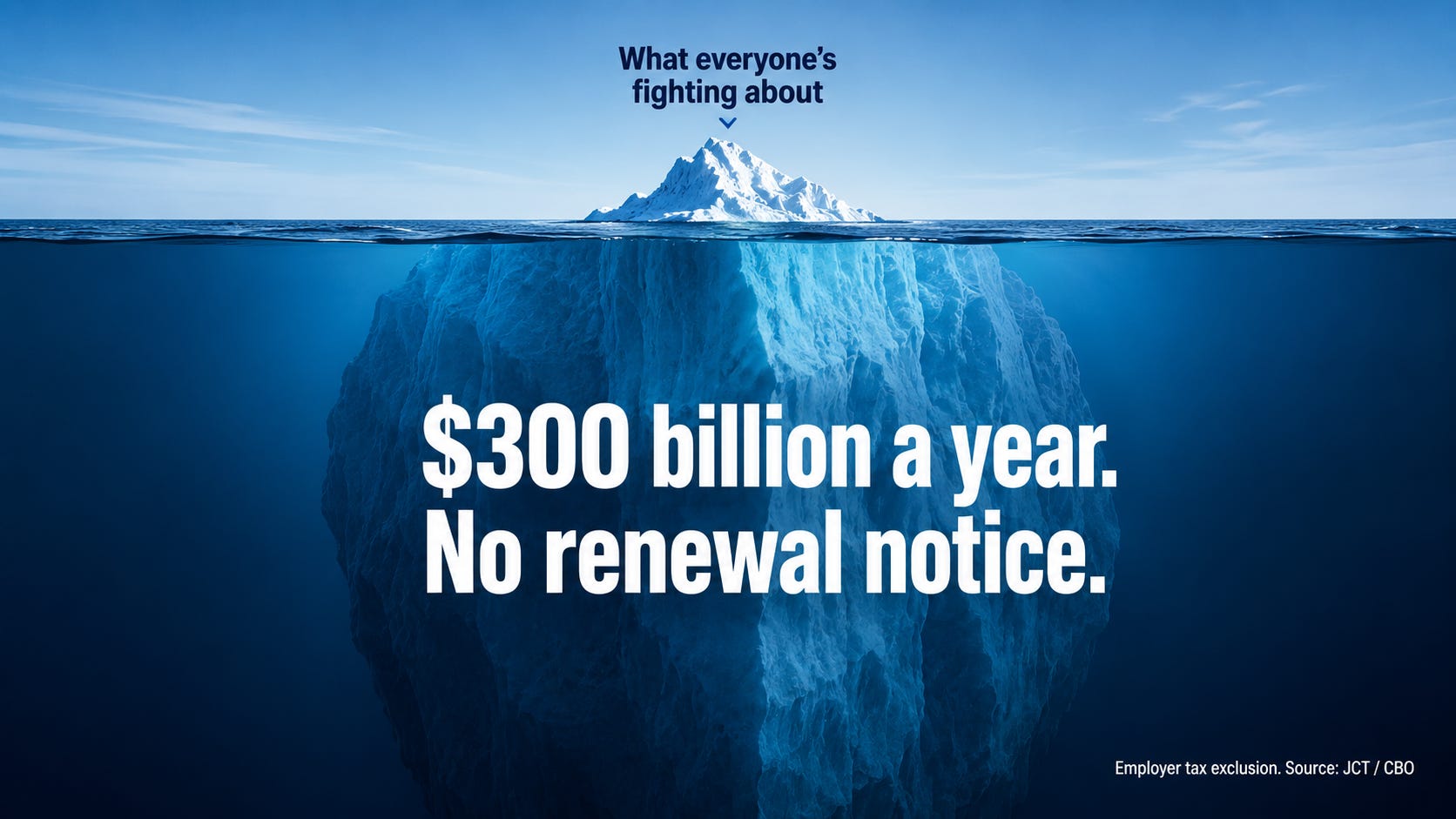

That arrangement rests on the largest health-related tax break in the federal budget, and it is the one nobody argues about on television. The tax exclusion for employer health benefits costs the federal government roughly $250 billion to $300 billion a year in revenue it never collects, depending on whether you count income taxes alone or income plus payroll taxes. It covers roughly 160 million people. It is bigger than the marketplace credit fight by a lot. Usually two to three times bigger, depending on the year and accounting method.

Put the two rooms side by side.

The marketplace subsidy is visible. It has a name, a vote, a sunset date, a cable segment. When it shrinks you feel it in one painful number and you get angry at a party. Good. Stay angry.

The employer exclusion is invisible. There is no renewal notice. It shows up as a flat paycheck and a vague sense that healthcare just costs a lot. It is also regressive, which is the polite word for upside down. A high earner at a big firm gets a fatter tax break on their coverage than a line cook at a small one.

And the part that should land on everyone the same way: Republican leaders cutting Medicaid are not putting this machine on the table, and Democrats expanding marketplace credits are not putting this machine on the table either. Each party runs a version of the healthcare fight that flatters its own crowd and leaves the big machine in the basement running.

The mechanism does not have a party. It is the same machine billing us in different rooms. One room sends a loud bill you can rage at. The other dips into your wages so quietly you thank the company for the benefit. Whoever decided the bigger subsidy should be the silent one knew exactly what that buys. Well, fuck that guy.

So, while the anger is fresh and useful, three things you can actually do.

One. Before you drop your marketplace plan because the renewal scared you, run your real number through KFF’s subsidy calculator. The 114 percent is a projection for an unchanged plan. Your figure depends on your income and age, and you may still qualify for more help than the notice suggests. Decide on the real number, not the panic number.

Two. If you get coverage through work and you feel secure doing this, find your total premium, not just your share. It is on your W-2 in box 12, code DD, or in your benefits portal. Look at the gap between what you pay and what the plan costs. That gap is money you earned. It went to a premium instead of your account. You are allowed to know that.

Three. When a candidate talks healthcare at you this year, listen for which room they are standing in. Extending the credits is the visible fight, and it matters. Touching the employer exclusion is the structural one, and almost nobody will say it out loud. Ask them about the second one, and watch them change the subject.

That is the tell. The bill you never see is the one they would rather you never ask about.