The 350-Home Line, and the Eleven Doors Cut Into It

The law banning Wall Street from buying your neighbor's house has a number in it, 350, and the homes it lets Wall Street keep buying do not count toward that number.

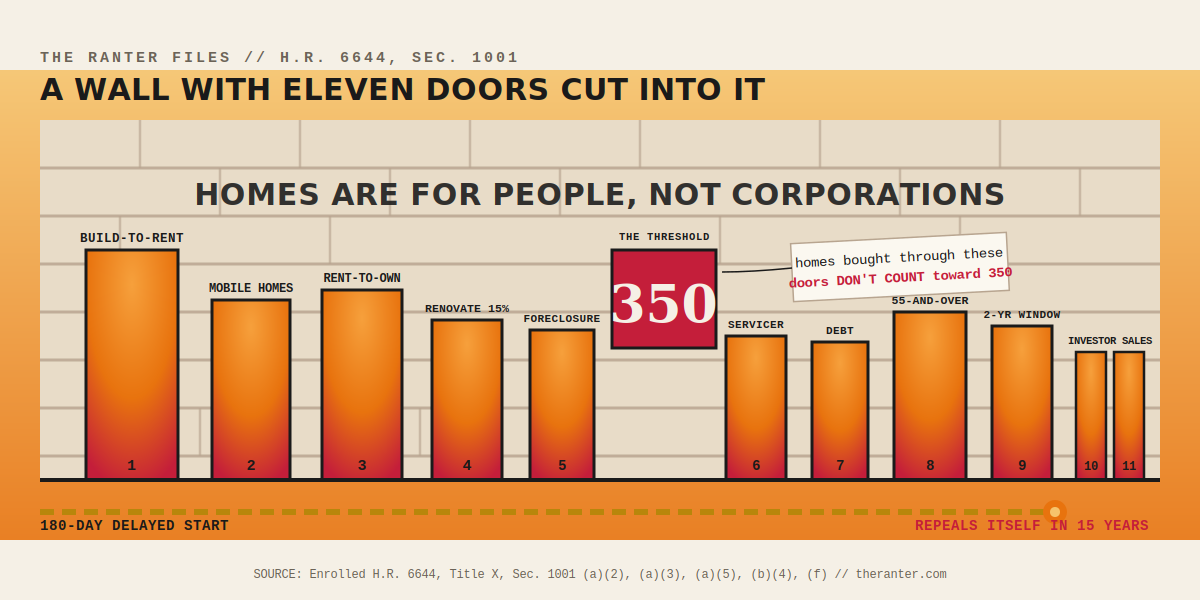

Section 1001 of the ROAD to Housing Act defines a “large institutional investor” as an entity that controls not less than 350 single-family homes. Below 350, the ban does not apply to you at all. Here is the part nobody is quoting: the statute says that count does not include any home bought through an “excepted purchase” after the law takes effect. So the homes the law lets you buy are the same homes that keep you under the line that would make you a “large institutional investor” in the first place. The threshold and the exceptions feed each other.

There are eleven excepted-purchase categories. A short walk through the ones doing the heavy lifting:

Build it instead of buying it. Newly constructed homes and build-to-rent programs are excepted (a(2)(A), (B)). The law tells institutional capital to stop buying existing houses off the market and start building the rentals. Within days, the trade press ran “New Housing Law To Send Institutional Investors Flocking To Build-To-Rent” (Bisnow).

Mobile home parks are not covered. The definition caps a “single-family home” at two units and excludes manufactured housing outright (a(5)). Private equity buying up mobile home parks, which is happening right now in Wisconsin and across the Sun Belt, sits entirely outside this ban.

Rent-to-own gets a federal safe harbor. Purchases under a “homeownership program” that charges rent, reports to credit bureaus, and offers “price concessions” are excepted (a(2)(D), (E)). The “slow flip” rent-to-own operators that consumer reporters keep exposing now have statutory cover.

Renovate-to-rent needs only 15 percent. Spend 15 percent of purchase price on rehab and a banned acquisition becomes an excepted one (a(2)(C)). On a $250,000 house that is $37,500.

The two-year buying window. For two years after the effective date, buying homes from any non-covered investor is excepted (a(2)(I)). That is a scramble to sweep up small-LLC inventory before it counts, not a cooling-off.

Treasury cannot close any of these. The rulemaking clause forbids the department from touching the definitions, the exceptions, or the 350 number (b(4)(B)). The holes are frozen into the statute.

This is the Cobra Effect, except nothing here is unintended. The classic version is a government pays a bounty on cobras, people breed cobras to collect it, and the policy produces more of exactly what it set out to kill. The twist is usually that nobody saw it coming. Here everybody could. The exceptions are not a loophole someone will discover in a courtroom three years from now. They are printed in the definitions, on the same pages as the ban, under a title that says homes are for people and not corporations. And the ban is not even permanent. Subsection (f) sets a 180-day delayed start and then repeals the whole prohibition 15 years later, so the wall everyone is cheering has a two-year buying window bolted to the front and a self-destruct timer on the back. When the build-to-rent subdivisions and the mobile-home-park rollups are still compounding in 2030 and someone asks how the corporate home-buying ban failed, the answer will be that it was legible the week it passed.

When someone forwards you the good news that Wall Street got banned from buying houses, you are the person who can send back the number. 350 homes, and the ones they keep buying do not count toward it. That is the whole trick in nine words. Hold it before the celebration starts.

Here is what I have learned to feel when a housing bill passes with a bow on it and both sides taking a victory lap. When the left claims it and the right claims it and everybody claims it, each caucus got its bite, and what is lying on the shoulder afterward is the part that was supposed to help actual people. They wrote “homes are for people, not corporations” across the top, cut the corporations eleven doors underneath, and set the whole thing to expire in fifteen years. Bipartisan. Everybody got what they wanted. None of it was you. Same time next week.

Source: Enrolled H.R. 6644, Title X, Sec. 1001 (a)(2), (a)(3), (a)(5), (b)(4), (f). // theranter.com