Everyone Left the Exchange. You Got the Bill.

Two ways the insurance cliff bills the people who are not in the headline.

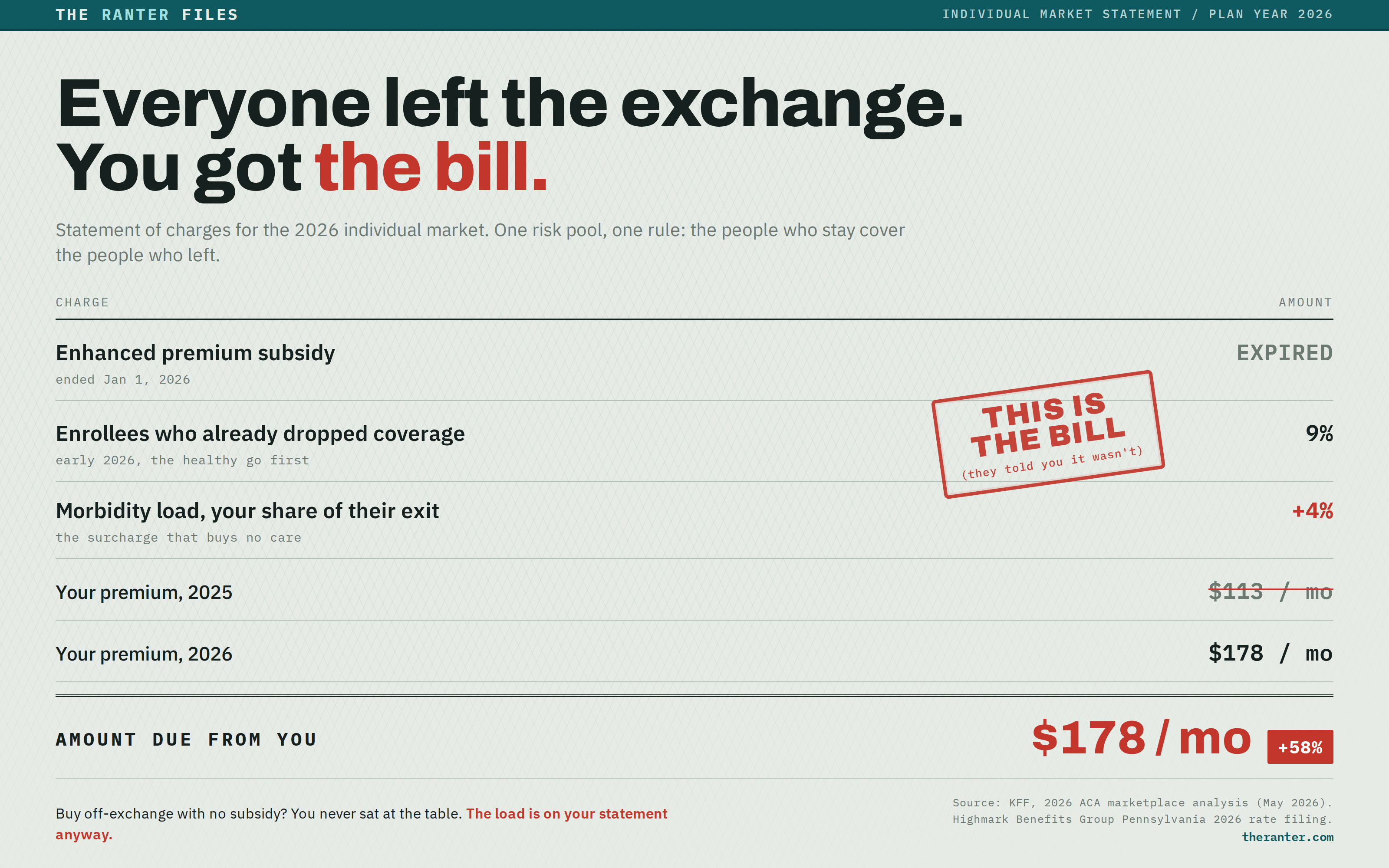

THE RANTER FILES

Highmark Benefits Group wrote a number into its 2026 rate filing in Pennsylvania and, I’ll give them this, named it in plain English. “Morbidity Impact from Expiration of Enhanced Premium Subsidies.” A factor of 1.040. Translate that out of insurance speak: a four percent surcharge tacked onto your premium that buys you not one minute of care. It sits inside a filing asking for a 17.93 percent average increase.

The surcharge pays for other people leaving. Highmark is charging the ones who stay, in advance, to cover the ones it expects to lose. Highmark did not invent it. CMS instructed 2026 insurers to assume the subsidies expire and write that into their rates. Across the market, that assumption added about four points to 2026 premiums, on top of a roughly 26 percent average increase.

The name for this is adverse selection, the oldest engine in the building. The healthiest leave, the pool left behind is older and sicker and costs more, the insurer raises the price on everyone still holding a policy, and the next-healthiest head for the door. The money owed for the people who left does not evaporate. It lands on whoever is still standing, including the off-exchange buyer who never qualified for a subsidy and never shows up in a coverage-loss story.

I buy mine off the exchange. Same load printed on my renewal letter, and I never had a subsidy to lose. I am paying for an exit I had no part in.

KFF found what enrollees actually paid: net premiums up 58 percent, from $113 a month to $178. That is under the doubling the early models warned about, and the smaller number is the worse news. It came in low because people ate the increase by dropping to thinner bronze plans or leaving entirely, and by early spring 9 percent of last year’s enrollees were already uninsured.

The second bill waits a year and goes off at a desk in April. The One Big Beautiful Bill Act, now Public Law 119-21, struck the cap on paying back excess premium credits, effective for tax year 2026. The old rule capped what you owed if you took too much subsidy up front. Starting with the coverage you hold right now, that cap is gone. Earn a dollar over 400 percent of the poverty line, from a bonus or a strong freelance quarter, and you repay the entire advance subsidy when you file in 2027.

Here is why it keeps happening, and why it does not belong to one team. Making the enhanced credit permanent scored at $335 billion over a decade, so Congress wrote it with a sunset, which kept that number off the official books. Too expensive to admit to, so they put it on a timer and nobody had to sign for the result. Fine. That is fine. Then on December 11, both parties’ fixes died the same afternoon by the same count. The Democratic three-year extension failed 51 to 48. The Republican plan to swap the subsidy for health savings accounts failed 51 to 48. The House had passed a three-year extension in January, 230 to 196, with seventeen Republicans crossing, and the Senate took the papers and set them down. The bipartisan Collins-Moreno compromise is a press release, not a law.

The claim that the surcharge is pure profit is contested. The medical-loss-ratio rule makes individual-market insurers spend at least 80 percent of premium dollars on care or rebate the difference, so a load matching a sicker pool is not pure profit. Read the same rule the other way, though. The share the insurer keeps is a percentage, not a fixed sum, so every dollar the premium climbs lifts the dollar value of that cut. The cap written to limit the take quietly hands the industry a stake in a bigger bill. And the fraud the other side points to did happen: CMS pulled roughly 1.5 million ineligible or unauthorized enrollments off HealthCare.gov last year. That is a real oversight problem, and a different lever than letting the whole subsidy lapse and surcharging the people who stayed.

Two things you can do this week. First, find your state’s 2026 rate filing, public on your insurance department’s site or through the SERFF system, and look for the morbidity or subsidy-expiration load. If you buy off-exchange with no subsidy, you are paying a surcharge for an exit you had no part in, and the rate-review comment window is where you say that on the record. Second, if you take advance credits, run your 2026 income against the 400 percent line now, while you can still steer it, because a dollar over later costs you the entire subsidy back.

You are holding the bill for the people who walked. Go find the line in your own filing, and say so on the record while the window is open.